SMM July 15:

Metal market:

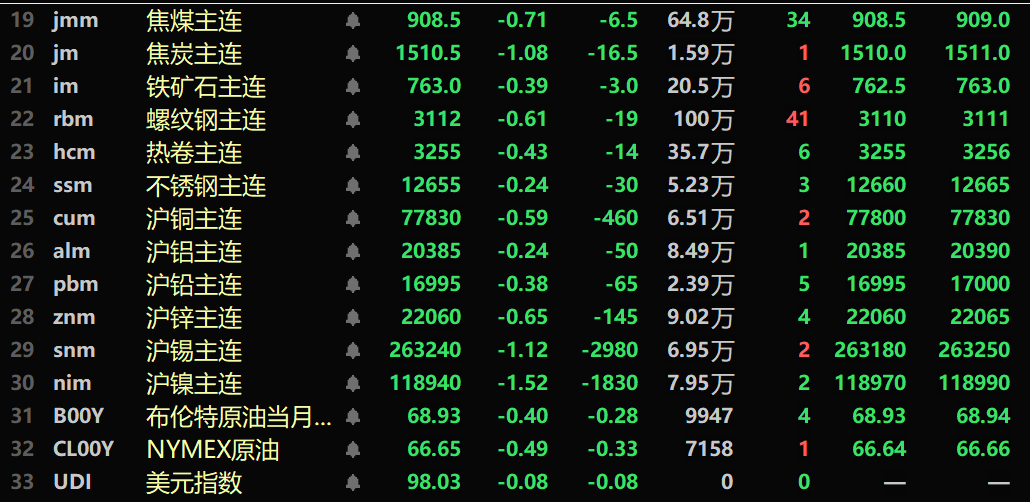

By midday close, base metals in the domestic market fell across the board, with SHFE nickel down 1.52%, SHFE aluminum down 0.24%, SHFE copper down 0.59%, SHFE lead down 0.38%, SHFE zinc down 0.65%, and SHFE tin down 1.12%.

Additionally, the most-traded cast aluminum futures fell 0.15%, while alumina rose 0.61%. Lithium carbonate dropped 2.1%, silicon metal gained 2.22%, and polysilicon increased 1.62%.

Ferrous metals series all declined, with iron ore down 0.39%, rebar and HRC down 0.61% and 0.43% respectively. Stainless steel fell 0.24%. For coking coal and coke, coking coal dropped 0.71% and coke declined 1.08%.

In the overseas market, as of 11:40, LME metals all fell, with LME aluminum down 0.1%, LME nickel down 0.39%, LME zinc down 0.49%, LME tin down 0.55%, LME lead down 0.55%, and LME copper down 0.01%.

For precious metals, as of 11:40, COMEX gold rose 0.16% while COMEX silver fell 0.84%. Domestically, SHFE gold gained 0.11% and SHFE silver edged up 0.01%.

By midday close, the most-traded Europe container shipping futures contract surged 8.27% to 1,553.6 points.

As of 11:40 on July 15, some futures midday quotes:

[ July 15 SMM Metal Spot Prices

Spot and fundamentals

Copper: Today, spot #1 copper cathode in Guangdong traded at a discount of 40 yuan/mt to a premium of 50 yuan/mt against the front-month contract, averaging a premium of 5 yuan/mt, up 35 yuan/mt from the previous day. SX-EW copper was quoted at a discount of 100-80 yuan/mt, averaging a discount of 90 yuan/mt, up 70 yuan/mt. The average price of #1 copper cathode in Guangdong was 78,040 yuan/mt, down 385 yuan/mt, while SX-EW copper averaged 77,945 yuan/mt, down 350 yuan/mt. Spot market: Guangdong inventory rose for two consecutive days as downstream demand remained sluggish ahead of contract rollover, keeping inventory elevated. Suppliers actively refused to budge on prices thanks to a significantly narrowed price spread between futures contracts... ] Click for details

Macro front

Domestic:

[NBS: H1 GDP up 5.3% YoY, national economy overcame difficulties and remained stable with positive trends] The National Bureau of Statistics (NBS) released H1 economic data. Preliminary calculations showed H1 GDP reached 66,053.6 billion yuan, up 5.3% YoY at constant prices. By sector, primary industry added value stood at 3,117.2 billion yuan (up 3.7% YoY), secondary industry at 23,905 billion yuan (up 5.3%), and tertiary industry at 39,031.4 billion yuan (up 5.5%). Quarterly data shows that China's GDP grew by 5.4% YoY in Q1 and 5.2% YoY in Q2. On a QoQ basis, GDP expanded by 1.1% in Q2. In H1, the industrial output above designated size nationwide increased by 6.4% YoY. Breaking down by sector, mining sector output rose 6.0% YoY, manufacturing output grew 7.0%, and the electricity, heat, gas, and water production/supply sector expanded 1.9%. Equipment manufacturing output surged 10.2% YoY, while high-tech manufacturing output grew 9.5% - 3.8 and 3.1 percentage points faster than the overall industrial output above designated size respectively. By economic type, state-controlled enterprises saw 4.2% YoY growth, joint-stock enterprises grew 6.9%, foreign-invested and Hong Kong/Macao/Taiwan-invested enterprises increased 4.3%, and private enterprises expanded 6.7%. By product category, output of 3D printing equipment, NEVs, and industrial robots jumped 43.1%, 36.2%, and 35.6% YoY respectively. In June, industrial output above designated size grew 6.8% YoY and 0.50% MoM. 》Click for details

[NBS: Consumption policies will continue to strengthen in H2 to halt property market decline and stabilize prices]Sheng Laiyun, Deputy Director of the National Bureau of Statistics, stated at a State Council press conference that China has implemented a series of policies this year to support domestic demand expansion, boost production, and improve circulation. NBS tracking data shows improvements in people flow, logistics, and capital flow. Local governments have adopted city-specific measures to stabilize the property market per central directives, with statistical data indicating significant progress. The property sector is generally moving toward halting decline and stabilizing, evidenced by narrowing sales declines in commercial housing, reduced price fluctuations across first-, second-, and third-tier cities (though overall price declines persist), improved funding channels for real estate enterprises with orderly debt resolution, and four consecutive months of inventory reductions. Sheng emphasized that while sales volume and prices remain below previous years' levels, the bottoming-out transformation is a normal process requiring greater efforts to stabilize the market. In H1, China's consumer market showed revitalization and positive growth momentum under consumption-boosting policies. H2 consumption growth will be supported by sustained positive factors from H1 and continued policy reinforcement. China's economic stability in H2 is underpinned by three factors: 1) H1's steady progress creating a solid foundation for annual targets; 2) long-term high-quality development trends and new growth momentum from structural rebalancing enhancing sustainable capacity; and 3) coordinated macro policies safeguarding stable economic operations. Based on a comprehensive assessment, China's economy is expected to maintain steady progress and improvement in H2. Click for details

[PBOC injects CNY173.5 billion via open market operations]The People's Bank of China (PBOC) conducted CNY342.5 billion of 7-day reverse repo operations today at an unchanged interest rate of 1.40%. With CNY69 billion of 7-day reverse repos and CNY100 billion of 1-year MLF maturing today, the net injection reached CNY173.5 billion.

US dollar update:

As of 11:40, the US dollar index fell 0.08% to 98.03. Market focus now shifts to the US June CPI data scheduled for release at 20:30 tonight. Economists surveyed project headline CPI to rise to 2.7% YoY from 2.4% previously, while core CPI is expected to accelerate to 3.0% from 2.8%. US President Trump again criticized Fed Chairman Powell, arguing interest rates should be at 1% or lower. US federal funds futures traders now price in a 50bps rate cut by year-end, with the first cut anticipated in September.

Data highlights:

Today's releases include Eurozone/Germany July ZEW economic sentiment indices, Eurozone June total reserve assets, US June headline/core CPI (unadjusted YoY), US July Empire State manufacturing index, Canada June headline/core CPI (unadjusted YoY), and Canada May manufacturing sales/new orders. Key events: State Council press conference on national economic performance; 2025 FOMC voter Susan Collins (Boston Fed President) speech; Fed Governor Bowman's welcome remarks at Fed-hosted conference; BOE Governor Bailey and UK Chancellor Rachel Reeves speaking at Mansion House dinner.

Crude oil update:

Both oil futures dropped slightly as of 11:40, with WTI down 0.49% and Brent down 0.4%. Persistent concerns over US trade tariffs continue to weigh on markets, as potential tariffs could slow economic growth, dampen global fuel demand, and drag oil prices lower.

OPEC Secretary General Haitham Al-Ghais stated (via RIA) that the organization expects "very strong" Q3 oil demand, followed by tightening supply-demand balance in subsequent months. Goldman Sachs raised its oil price forecast for the second half of 2025 (H2 2025) on Monday, citing risks of supply disruptions, declining oil inventories in OECD countries, and Russia's production restrictions.

A preliminary survey showed US crude and gasoline inventories are expected to decline last week, while distillate stocks are anticipated to increase. Prior to the release of weekly inventory data, the average forecast from five surveyed analysts indicates US crude inventories are expected to fall by approximately 1.6 million barrels for the week ending July 11. The American Petroleum Institute (API) will publish its weekly inventory report at 4:30 Beijing time on Wednesday, followed by the US Energy Information Administration (EIA) releasing its report at 22:30 Beijing time on the same day. (Comprehensive coverage by Wenhua)

Spot market overview:

►Benefiting from a significant narrowing of the price spread between futures contracts, suppliers actively refuse to budge on prices to sell goods [SMM South China Copper Spot]

Other non-ferrous metal spot market updates will follow later—please refresh for details.